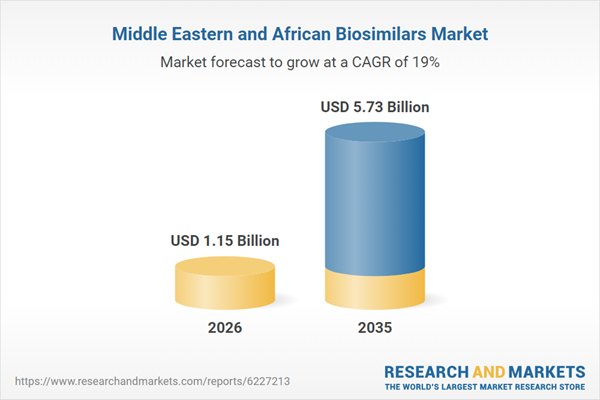

The Middle East and Africa biosimilars market is poised for significant expansion, with projections indicating a surge from USD 1.15 billion in the current year to USD 5.73 billion by 2035, reflecting a robust Compound Annual Growth Rate (CAGR) of 19%. This impressive growth trajectory is fueled by escalating healthcare investments, a rising prevalence of chronic diseases such as diabetes and cancer, and supportive regulatory frameworks in key regional economies like Saudi Arabia, the UAE, and South Africa.

The urgent demand for affordable biologic alternatives, particularly in resource-constrained areas where the high cost of original biologics often limits patient access to crucial treatments for chronic illnesses, serves as a primary driver for market growth. The market is expected to accelerate further as patents for original biologics expire, paving the way for biosimilars that offer comparable safety and efficacy at more accessible price points. While the biologics sector has witnessed substantial growth due to its effectiveness in managing chronic diseases, the associated high costs present considerable financial and healthcare challenges. Consequently, developers are actively exploring innovative strategies to produce more affordable biologic products without compromising on quality, aiming to optimize their investment returns.

Several strategic factors are underpinning this market expansion. These include the increasing prevalence of chronic conditions like cancer, diabetes, and autoimmune disorders, coupled with a growing demand for cost-effective biologic options. Government initiatives, such as streamlined regulatory pathways for biosimilars, are also playing a crucial role. Furthermore, the expiration of patents for major drugs like Herceptin and Rituxan is enabling local manufacturers to rapidly broaden their product portfolios. The region’s low-cost manufacturing capabilities, skilled workforce, and strategic partnerships with global firms are positioning the Middle East as a prominent exporter in the biosimilars sector.

Despite this promising growth, the Middle East and Africa biosimilars market faces several challenges that could impede faster adoption. High development costs, complex manufacturing processes demanding stringent quality controls, and the inherent risks of immunogenicity or structural variability create significant entry barriers, particularly for smaller market players. Regulatory complexities, including evolving guidelines and the necessity for comparative clinical trials, often lead to delayed approvals. Additionally, insufficient domestic production and R&D infrastructure contribute to import dependency and potential supply disruptions. Market access issues, such as intense competition from branded generics, pricing pressures, and patent litigations from originator companies, further constrain market expansion.

Within the market, monoclonal antibodies currently dominate, holding nearly 55% of the total share in the Middle East and Africa. This leadership is primarily due to their extensive use in treating chronic conditions like cancer, rheumatoid arthritis, and various autoimmune disorders. However, the peptide segment is anticipated to experience the fastest CAGR throughout the forecast period.

In terms of therapeutic areas, oncological disorders currently command the largest share of the Middle East and Africa Biosimilars Market. This trend is reinforced by an aging population, lifestyle changes, and advancements in diagnostic techniques, all of which underscore the need for affordable treatments, particularly for expensive monoclonal antibody therapies. This segment, therefore, presents attractive growth opportunities for biosimilar developers. The hematological disorders segment is also projected to achieve a higher compound annual growth rate during the forecast period.

#BiosimilarsMarket #MEAHealthcare #PharmaceuticalTrends #ChronicDiseases #AffordableMedicines #Biologics #MarketGrowth #HealthcareInvestment #MonoclonalAntibodies #OncologyTreatment